The owners of the 320-unit Bishan Park Condominium each stand to receive proceeds ranging from $1.9 million to $2.3 million from the en bloc sale.PHOTO: ERA

SINGAPORE - Bishan Park Condominium in District 20 has been launched for collective sale, with the owners expecting offers of around $680 million to $688 million, marketing agent ERA Realty said on Tuesday (Sept 24).

Located at 14 Sin Ming Walk, the estate comprises five blocks of 10 storeys each, totalling 320 units. The 99-year leasehold development, with 71 years left on its lease, sits on 269,796 square feet (sq ft) of land area with a plot ratio of 2.1.

After factoring in a 7 per cent bonus balcony gross floor area (GFA), the land rate works out to around $1,122 per square foot per plot ratio, ERA said.

An estimated $70 million to $75 million will be required for the intensification of the site and also to top up to a fresh 99-year lease, subject to approval from the relevant authorities.

The owners stand to receive sales proceeds ranging from $1.9 million to $2.3 million for each unit from the en bloc sale.

More than 80 per cent of the condo's subsidiary proprietors by share value and strata area have signed the collective sale agreement, said Stanley Koo, ERA's division director.

Bishan Park Condominium is 400 metres from the upcoming Bright Hill MRT Station on the Thomson-East Coast Line. It is a 15-20 minute drive from the central business district and the Orchard Road shopping belt, and is also connected to major expressways.

Amenities and facilities nearby include Bishan Park and Gardens, the Upper Thomson Road stretch of eating establishments, as well as the Thomson Plaza and Junction 8 malls. Also in the vicinity are schools such as Ai Tong School, CHIJ St Nicholas Girls' School, Ang Mo Kio Primary School, Raffles Institution and Catholic High School.

The proposed residential redevelopment will not require a pre-application feasibility study, ERA noted.

Condominiums in the Tanjong Rhu area in Singapore. In the first eight months of this year, 68 condo units in Singapore were sold for $10 million and more each, the highest tally since the corresponding period of 2008. The surge was fuelled by increased demand from Chinese millionaires seeking safe-haven assets, according to OrangeTee & Tie.PHOTO: REUTERS

Sales of Singapore apartments worth at least $10 million each have hit an 11-year high, fuelled by increased demand from Chinese millionaires seeking safe-haven assets, said property consultancy OrangeTee & Tie.

Investors have long viewed Singapore as an island of stability that attracts the super rich from its less developed South-east Asian neighbours, as well as multi-millionaires from mainland China.

In the first eight months of this year, 68 condominium units in the wealthy city state were sold for $10 million and more each, the highest tally since the corresponding period of 2008.

Sales of such apartments also exceeded the numbers racked up for each full year from 2011 to last year, the consultants' analysis of transaction data shows.

Some buyers may have been seeking an alternative to rival financial hub Hong Kong, which has been hit by protests, while others may have been moving funds from China after its yuan currency was devalued in a trade war with the United States, an OrangeTee expert said.

"This may explain why we have observed more foreign buyers, especially mainland Chinese, coming into Singapore lately," said Ms Christine Sun, head of research and consultancy at OrangeTee.

Mainland Chinese are the biggest group of foreign buyers of Singapore luxury homes.

In Singapore's prime districts, Chinese citizens bought 76 apartments worth more than $5 million each in the period from January to last month, compared with 75 purchases by Singaporeans, data until last Thursday shows.

Expensive apartments in premium neighbourhoods are mainly bought by foreigners, because at such high prices Singaporeans have the option to buy landed property, such as bungalows and mansions.

Singapore does not allow foreigners to buy landed homes, except for those that are on the resort island of Sentosa.

"We do see that even though the stamp duties have increased... we are still seeing people putting big money on these apartments, predominantly more for stability than anything else," said Mr Leong Boon Hoe, chief operating officer of high-end property agency List Sotheby's International Realty.

He was referring to measures Singapore adopted last year to cool its real estate market, such as hiking additional stamp duties for foreign buyers to 20 per cent from 15 per cent. "They are parking their money here - they know that the Singapore dollar won't depreciate overnight," he said.

Fun fact: there are roughly 70,000 flats that are halfway through their lease, and will face lease expiry in the next 50 years. Before you buy one of them, we’d like to remind you that unlike STOMP articles, buying a home is a MAJOR life decision and shouldn’t be taken lightly. Consider EVERYTHING before you pull the trigger.

It’s getting easier for Singaporeans to buy old flats, and they are tempting

Thanks to the new CPF rules, you can now use the money in your CPF Ordinary Account (CPF OA) to buy a flat even if there’s just 20 years on the lease*. That doesn’t just impact the immediate affordability; it means there will still be some value in your 40+ year old flat, should you try to resell it later.

Of course, old flats are also more tempting, location wise. Have you seen what typically goes on offer at a BTO launch? New flats tend to be in less mature districts, and some of them (looking at you, Tengah) are so underdeveloped, National Geographic might pay you to look for lost tribes in the area.

An old flat, on the other hand, has more amenities nearby. It can mean living next to a legendary eatery, or minutes from bus stations, MRT stations, Sheng Siong, etc.

But there are some serious considerations that should be addressed; issues such as:

Your flat won’t be as much help to your retirement fund

You can’t count on SERS and VERS

Those amenities may not last as long as your flat

HIP or no HIP, maintenance is likely to be an issue

You better have a plan in case you live too long

*So long as the lease will last until the youngest buyer is 95 years old

Let’s go over these slowly, shall we?

1. Your flat won’t be as much help to your retirement fund

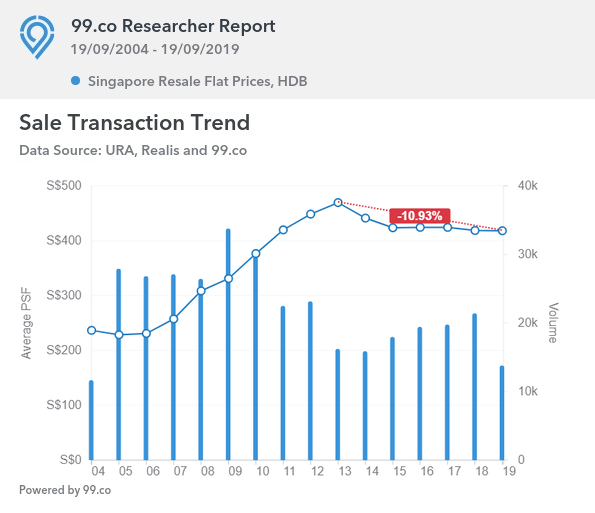

We’re long past the days when people would pay crazy prices for resale flats. Also, you can mostly forget about Cash Over Valuation (COV) these days. Sure, it still happens and there are occasional million-dollar flats; but for the most part, this is what resale flat prices are up to these days:

Notice how it’s flattening out, like the hopes of resale owners everywhere

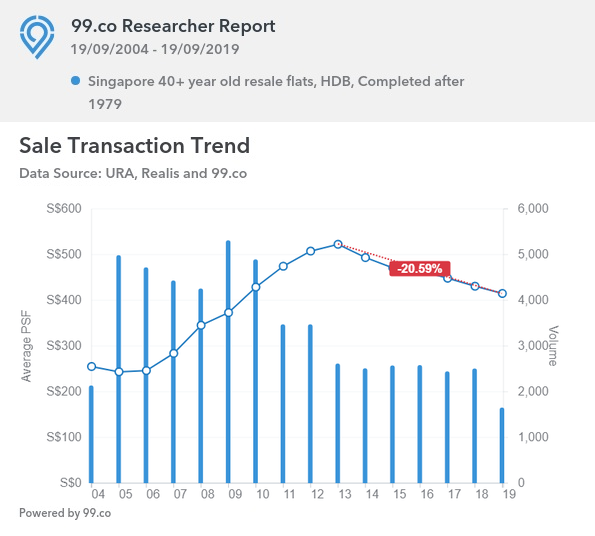

Just to be more specific, here’s what it looks like for flats completed in 1979 or earlier:

Even if you can resell a flat that was 40+ years old when you bought it, you shouldn’t expect it to help your retirement fund much. Singaporeans are just much more aware – and sensitive – about lease decay today. And unless you own a very rare type of flat – like a maisonette, or a unit with 1970’s kitchen decor that doesn’t make you vomit – you might see a capital loss.

So if you’re buying an old flat, don’t think of it as a future retirement fund. Look for alternative assets to fulfill that purpose. And treat the flat as a pure overhead – it’s a roof over your head and nothing more.

2. You can’t count on SERS and VERS

Only around five percent of estates will qualify for the Selective Enbloc Redevelopment Scheme (SERS). We wouldn’t count on it, unless your flat is in a particularly visible and iconic location.

If your flat is thew sort that appears on postcards and is visible from major roads, that’s a location that might be SERS-worthy. But if the flat is just tucked away in a quiet corner (i.e. the vast majority of them), then you probably won’t be a getting a new flat with a 99-year top-up.

As for the Voluntary Early Redevelopment Scheme (VERS), it hasn’t happened yet; but we know the payouts won’t be as generous as SERS. If its pegged to market value, that could mean returns are barely enough to buy another, smaller flat. And by the time you return the CPF money used, the pay out might be enough for maybe one char siew bao, if you agree to share.

It also takes 80 per cent consensus for VERS to happen. That’s hard enough to get in a condo, let alone in a property with as many owners as an HDB flat.

3. Those amenities may not last as long as your flat

Wow, my regrets taste exactly like this $39 gluten-free artisanal chicken rice

If you’re going to risk buying an old flat for the amenities, make sure those amenities really matter. Having an MRT station or good school nearby counts; having a famous kolo mee stall nearby doesn’t.

Remember that even the oldest amenities can go the way of Chin Mee Chin Confectionery. In fact, we’d suggest that for any property – especially in older areas, which are typically targeted for redevelopment – you check the URA Master Plan.

Sometimes, even that doesn’t help.

In Tiong Bahru, for instance, the area suffered death by cappuccino. Gentrification replaced older amenities with upscale hipster amenities, which many of the older residents there can’t afford or have no interest in. Are you okay to replace your kolo mee with pumpkin-spiced avocado whatever? Because that may happen.

The older the area, the more likely it is that sweeping changes are due; if not organically, than through deliberate redevelopment. Factor in that risk, when buying such an old flat.

4. HIP or no HIP, maintenance is likely to be an issue

Our prior article addressed misconceptions about HIP. This isn’t a magic wand that HDB will point at your flat, and instantly erase month old stains in the flooring, or correct sagging toilet doors. HIP handles the essentials; everything else comes down to renovation and maintenance out of your old pocket.

That means you’re likely to spend much more on renovations, compared to an brand new BTO flat. And simple age causes issues that are elusive to fix – the wafting scent of ageing pipes in the toilet, the unusually low water pressure from a tap because of a leak…somewhere, the odd stains that keep appearing no matter how many times you patch them, etc.

Be prepared to spend more as your flat breaks down like an alcoholic’s liver.

5. You better have a plan in case you live too long

We’re pretty fond of our mortgage, we’ve paid it so long it’s old enough to buy our grandson a beer

Based on all the insurance ads and CPF planning messages, we surmise that Singaporeans now have a lifespan than would shock a vampire. We do, after all, have the longest life expectancy in the world (yes, even longer than Japan. All that kolo mee must be good for the heart).

But in any case, do pause to think: what if your 40+ year-old flat turns out to have a shorter lifespan than you? It’s not as if you’re in a good position to sell it and move, in the twilight of your life. And should you outlive your flat at the age of, say, 80+, it’s rather difficult to find the funds for a new home at that point.

So before you buy that old flat, make sure it will last till the end of your life, or that you have a plan for when it doesn’t. And remember, moving to Thailand tends to sound a lot less appealing once you’re past 75.

If you’re a first time homeowner, you might just find deciphering your HDB floor plan a little tricky to navigate. In this article, we break down the different symbols and explain to you what they mean. Plus, we’ve also included some tips on key considerations to be mindful of when looking at your HDB floor plan. (Cover image credits) Read on to find out more!

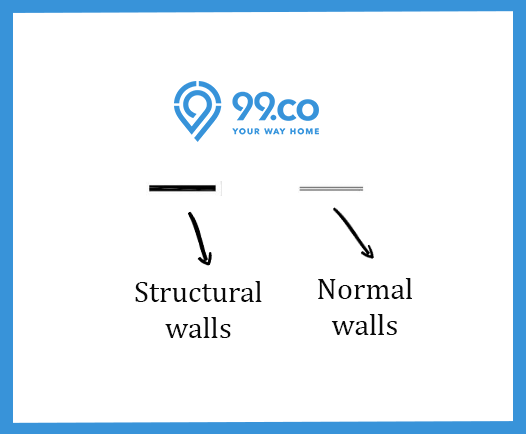

#1: Walls

Structural walls refer to foundation walls or pillars that hold the apartment together. These are strictly non-hackable – so keep that in mind if you have big plans for the open-concept kitchen or walk-in wardrobe of your dreams. With normal walls, on the other hand, you’ll get more leeway – simply get the necessary approval from HDB and you’ll be able to go ahead with your hacking.

#2: Doors

Solid lines denote doors that have been provided; dotted lines refer to doors that you’ll have to build in yourself. Do also pay attention to the arc in the HDB floor plan, which indicates the direction in which the door swings. As for folding doors, these are commonly found in bathrooms and service yards.

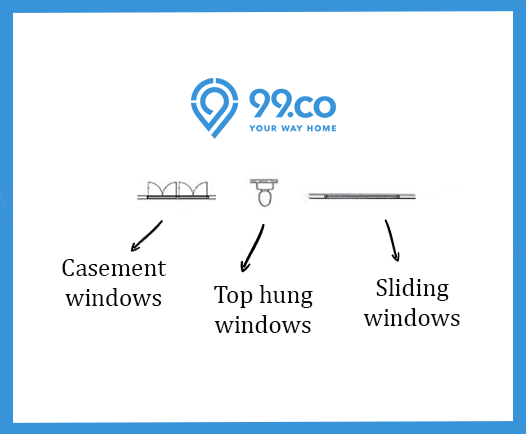

#3: Windows

Casement windows swing outwards when opened, top hung windows are small windows located at the top of the wall (typically only present in bathrooms), and sliding windows are, well, sliding windows!

Beyond reading the HDB Floor Plan

Now that you know how to read the symbols on your HDB floor plan, let’s move on to talking about some other issues to consider:

1) Is the layout boxy, or are there oddly-shaped corners?

To maximise space and make your life easier when you’re furniture-shopping, look for boxy layouts. You don’t want to have too many oddly-shaped corners, as these are essentially dead space (unless you’re planning on custom-making furniture!)

2) The size of your master bedroom

Some flats come with master bedrooms that are significantly larger than the other rooms; others come with master bedrooms that are only slightly larger. Depending on how you want to use your space, give some thought as to which arrangement you prefer.

If you’ll be spending a lot of time in your other rooms or using these to store large and bulky items, you might be fine with a layout that allocates the space more evenly. Otherwise, if the bulk of your time will be spent in your master bedroom, it makes sense to look for a layout that allocates more space to this room!

3) Placement of toilets

Not all HDB flats have one toilet attached to the master bedroom, and the other attached to the kitchen. Make sure you double-check your HDB floor plan to see what’s the situation like, and as with the above, think about whether this makes sense to your desired living arrangements.

This information can guide you on the financial planning for your resale flat purchase, and help you to determine the suitable flat choices within your budget, making it easier when it comes to searching for your flat.

To work out a comprehensive financial plan, be sure to consider the following:

Cash and CPF savings

Housing loan

CPF Housing Grant Scheme

Payments involved

For a start, you can use our financial tools to determine your current financial position and how much you can borrow for your flat purchase. If you require further guidance and details, please refer to more information on financing a flat purchase.

Cash and CPF savings

You will probably use both cash and CPF savings for your flat purchase. Your resale flat financial planning should therefore cover:

How much cash is required

Amounts that can be paid using CPF savings

Cash Savings:

You must use cash for the following payments:

Deposit to seller (a maximum of $5,000, paid in 2 stages: the option fee, and the deposit)

Part of the initial payment (if you take a bank loan, or have insufficient CPF savings)

Amount not covered by CPF savings and eligible housing loan amount

Cash proceeds from disposing the last flat if you are taking a second HDB loan*

*If you are taking a second HDB loan to buy the resale flat, you will need to set aside part of the cash proceeds from the disposal of the existing or previous flat. That amount will be used to right-size the loan amount for your second HDB loan.

You will also need to set aside cash savings for other expenses such as furnishings, renovation, and some other costs and fees payable .

CPF Savings:

The savings in your CPF Ordinary Account (OA) can be used for:

Initial payment in whole or in part (depending on whether an HDB or bank housing loan is used)

Partial or full payment for the flat purchase

Monthly mortgage instalments

However, do take note that there is a CPF withdrawal limit on the amount of CPF savings that can be used for your flat purchase. Once that limit is reached, you will not be able to use more CPF savings to pay for the flat.

Flat buyers taking an HDB housing loan will have the option of retaining up to $20,000 CPF savings in each buyer's Ordinary Account (OA). The rest of the available CPF OA balance must be used to pay for the flat purchase.

From 10 May 2019, the total amount of CPF that can be used for your flat purchase will depend on the extent the remaining lease of the property can cover the youngest buyer to the age of 95. Details on the use of CPF savings for the flat purchase are shown below.

Flat applications received on or after 10 May 2019:

Remaining lease of property is at least 20 years and can cover youngest buyer until at least age of 95

CPF Usage

Yes

Buyer can use CPF to pay for the property up to the Valuation Limit

No

Use of CPF will be pro-rated based on the extent the remaining lease of the property can cover the youngest buyer to the age of 95. This will help buyers set aside CPF savings for their housing needs during retirement (e.g. a replacement property).

For information on the use of your CPF to buy a flat, you may use the online calculator at CPF Board’s website.

Flat applications received before 10 May 2019:

Remaining lease of property

CPF Usage

60 years or more

Buyer can use CPF to pay for the property up to the Valuation Limit^ (VL)

30 years to less than 60 years

Buyer can use CPF if the remaining lease of the property covers the youngest buyer until at least the age of 80

Total amount of CPF that can be used is capped at pro-rated VL

^The VL is the lower of the purchase price or the property value at the point of purchase. Usage beyond the VL (up to applicable limits) is allowed if the property buyers have accumulated their Basic Retirement Sum.

For further enquiries on the use of your CPF to buy a flat, please contact CPF Board Service Line at 1800-227-1188.

Information on the remaining lease of an HDB block is available on the HDB Map Services under "Housing".

Housing loan

To help you finance your flat purchase, you may choose to get a housing loan from HDB or a housing loan from the financial institutions (FIs)regulated by the Monetary Authority of Singapore.

To take on a housing loan, you need to meet the eligibility conditions and credit assessment criteria. You must also take note of these financing requirements:

Financing requirements:

If you take on a housing loan from HDB

You must have a valid HDB Loan Eligibility (HLE) letter when the sellers grant you the OTP.

The HLE letter will inform you of the loan amount you can get from HDB. Do exercise prudence and take on a loan amount that you can service comfortably over the loan tenure.

If you take on a housing loan from a Bank

You must obtain a Letter of Offer from the FI before you exercise the Option to Purchase.

Housing Loan From HDB:

We provide housing loans at concessionary interest rate to eligible flat buyers. These loans are subject to credit assessment and the prevailing eligibility conditions.

If you wish to get an HDB housing loan, you need to first apply for and obtain an HDB Loan Eligibility (HLE) letter. The HLE letter will inform you of the amount of loan you can get, based on your financial situation. As a good practice, obtain an HLE letter before you start searching for a flat, as knowing your housing loan amount will help you to calculate your budget to buy a flat.

If you take a housing loan from HDB, do note the following:-

You will need to have a valid HDB Loan Eligibility (HLE) letter when you book a new flat from HDB, or obtain an Option to Purchase from a resale flat seller

When you take a housing loan from HDB, you can later refinance your loan with another housing loan from a bank. However, if you take a housing loan from a bank, you will not be allowed to refinance your loan with a housing loan from HDB

For a second HDB concessionary housing loan, the loan quantum will be right-sized by utilising the CPF monies refunded and some of the cash from the disposal of your current/ previous flat

For resale flat applications submitted to HDB from 28 Aug 2018, flat buyers taking an HDB housing loan will have the option of retaining up to $20,000 CPF savings in each buyer's Ordinary Account (OA). The rest of the available CPF OA balance must be used to pay for the flat purchase.

For resale flat applications submitted to HDB on or after 10 May 2019:

Buyers who buy a flat with a remaining lease that can cover the youngest buyer till the age of 95 and above, the HDB housing loan amount that they may take will be up to 90% of the lower of the flat’s purchase price or value (“90% loan-to-value”).

Buyers who buy a flat with a remaining lease that does not cover the youngest buyer till the age of 95, the HDB housing loan amount that they may take will be pro-rated from the 90% loan-to-value limit.

You can click on the following links to use the online calculators to compute the allowable CPF usage and the HDB housing loan:

You can choose to finance your flat with a housing loan from the Financial Institutions (FIs) regulated by the Monetary Authority of Singapore (MAS). If you take a housing loan from an FI, you will not be allowed to refinance your loan with a housing loan from HDB.

When choosing a housing loan from an FI, assess the different housing loan packages offered by the FIs thoroughly and weigh your options carefully. Some key terms and conditions to look out for include lock-in periods, interest rates, and other financial considerations.

If you take a housing loan from an FI, do note the following:-

You must have a valid Letter of Offer before you exercise the Option to Purchase for the HDB resale flat

You will not be allowed to refinance your loan with a housing loan from HDB

You may be eligible for CPF housing grants, which are housing subsidies that the government gives to eligible Singapore Citizens. They can be used for a flat’s initial payment and for reducing the housing loan amount.

The main payments you need to make for a resale flat purchase are as follows:

Deposit to seller (option fee and deposit)

Initial payment

Cash payment for balance purchase price (if applicable)

There are also additional costs and fees that you need to be aware of.

Deposit to Seller:

This amount can be negotiated with the seller and is taken off the resale price.

Amount to Pay

Payment Mode

When to Make Payment

Up to $5,000 in total, paid in 2 stages.

Cash

1) Granting of OTP

Up to $1,000 is paid as the option fee.

2) Exercising of OTP

A deposit of up to $4,999 (cap of $5,000 minus the option fee amount) is paid.

Initial Payment:

You make the initial payment after acknowledging the resale documents in the HDB Resale Portal. The amount is based on the resale price or market valuation of the flat, whichever is lower, as well as whether you are:

Taking an HDB housing loan

Not taking any housing loan

Taking a bank loan

Housing Loan Type

Initial Payment

Mode of Payment

When to Pay

HDB loan/ Not taking any housing loan

10% of the purchase price

CPF

You can use your CPF OA savings (including CPF Housing Grant if eligible) to make the initial payment up to the full 10%. If your CPF OA amount is insufficient, the balance is to be paid in cash.

If you intend to use more than 10% of the purchase price of the flat from your CPF, you must have this amount available in your CPF account before submitting the resale application. Additionally, do note that flat buyers taking an HDB housing loan will have the option of retaining up to $20,000 CPF savings in each buyer's Ordinary Account (OA). The rest of the available CPF OA balance must be used to pay for the flat purchase.

Online withdrawal of your CPF monies after you confirm your Financial Plan through the HDB Resale Portal

Cashier's Order

At the resale completion appointment

Bank loan

25% of purchase price for loan ceiling of 75%

CPF

You can use your CPF OA savings (including CPF Housing Grant if eligible) to make the initial payment up to 20%. If your CPF savings is insufficient, the balance is to be paid in cash.

Please check with the bank for the payment schedule for your bank loan

Cash (minimum of 5%)

45% of purchase price for loan ceiling of 55%

CPF

You can use your CPF OA savings (including CPF Housing Grant if eligible) to make the initial payment up to 35%. If your CPF savings is insufficient, the balance is to be paid in cash.

Cash (minimum of 10%)

Cash payment for balance purchase price:

The cash payment for balance purchase price only needs to be paid when the resale price is higher than the market valuation.

Amount to Pay

Housing Loan Type

Payment Mode

When to Make Payment

The difference between the resale price and the market valuation

HDB loan/ Not taking any housing loan

Cashier's Order

At the resale completion appointment

Bank loan

Cash

Please check with the bank for the bank loan payment schedule

{kind=link}